Is Dangote refinery really worth $50 billion?

- May 11, 2026

Aliko Dangote wants investors to believe his refinery is worth more than the initial $20 billion estimate ahead of a planned listing on the Nigerian Stock Exchange (NGX) slated for June.

According to a Bloomberg report, Dangote could sell up to 10% of the refinery in a Nigerian initial public offering this year, implying a valuation of as much as $50 billion. The company could later pursue a secondary listing in London.

A premium valuation as high as $50 billion would place the Lagos-based refinery among the most valuable refining businesses in the world, despite the fact that the facility is still ramping up production and has yet to consistently operate at full capacity.

The refinery has already transformed Nigeria’s fuel market. Long dependent on imported gasoline despite being Africa’s largest oil producer, Nigeria is now exporting refined products, including jet fuel to Europe.

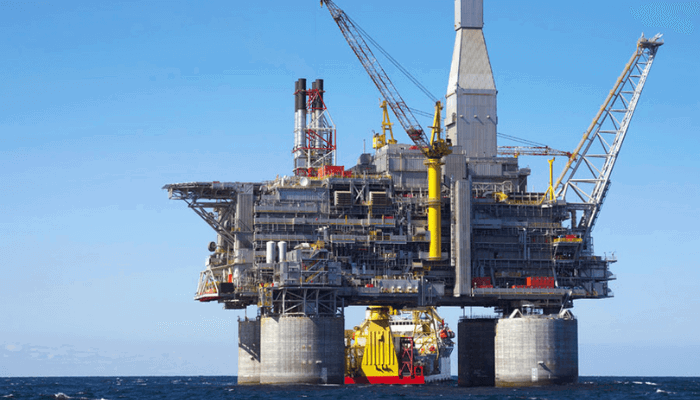

There is no doubt the refinery is a landmark project. At 650,000 barrels per day, it is the largest single-train refinery in the world. It has the potential to reshape fuel trade across West Africa and reduce the billions of dollars Nigeria spends annually importing petroleum products.

But investors are likely to ask a more immediate question: does the business today justify a $50 billion price tag?

That question becomes sharper when compared with some of the world’s biggest and most established refineries.

The Galveston Bay Refinery in Texas, owned by Marathon Petroleum, processes roughly 630,000 barrels per day, close to Dangote’s stated capacity. BP sold the refinery in 2013 for about $2.4 billion, though the site later underwent more than $1 billion in upgrades.

In South Korea, S-Oil operates the Onsan Refinery, which can process nearly 670,000 barrels per day. The entire company has recently been valued by the market at under $10 billion.

The Yeosu Refinery, run by GS Caltex, can process up to 800,000 barrels daily and serves major export markets across Asia. Valuation estimates tied to the broader business sit near $12 billion.

Then there is the Ruwais Refinery, operated by ADNOC. With capacity approaching 1 million barrels per day and years of operational history, ADNOC Refining was valued around $15 billion in a 2019 deal involving Austria’s OMV.

The biggest comparison is often the Jamnagar Refinery in India, owned by Reliance Industries. Jamnagar processes roughly 1.4 million barrels per day, more than double Dangote’s capacity, and is widely considered the world’s largest refining complex.

Against those benchmarks, Dangote’s target valuation appears ambitious.

Part of the skepticism comes from the refinery’s operational reality. Although production has started, the plant is still stabilizing operations. Refining is not simply about installed capacity. Investors care about how much crude a refinery consistently processes, how efficiently it converts fuel products, and whether it can maintain healthy margins through volatile oil cycles.

New refineries also face steep early costs. Maintenance, financing and supply chain adjustments can weigh heavily before operations settle into predictable patterns.

Dangote supporters argue the comparison with older refineries misses the point.

Unlike the United States, Europe or parts of Asia, Africa remains heavily dependent on imported fuels. Nigeria alone has spent decades importing gasoline while its state-owned refineries deteriorated. Demand for refined products across the continent continues to grow alongside urbanization and population increases. That gives Dangote a strategic advantage many older refineries no longer enjoy.

The refinery is also more than a standalone fuel plant. It is tied to petrochemicals, fertilizer production and port infrastructure within Dangote’s industrial network. Supporters say investors are buying into a broader energy and manufacturing ecosystem rather than a refinery alone.

The business tycoon’s plan to build a similar refinery in East Africa could be a factor to consider for investors looking at the long term.

Even so, a $50 billion valuation would still demand exceptionally strong future earnings.

For comparison, some publicly traded global refining companies with multiple assets, decades of operating history and diversified businesses trade below that level. Investors will likely examine the refinery’s debt burden, utilization rates, crude sourcing arrangements and export economics before accepting Dangote’s numbers.

The timing of the planned listing may also matter. Refining margins have strengthened in recent years because of tighter global fuel supplies after refinery closures during the pandemic and disruptions tied to the war in Ukraine. Higher oil prices and stronger fuel demand have improved the outlook for large export refineries.

Dangote may be betting those conditions hold long enough to secure a premium valuation.